In February, we published the Q1 Data Center Outlook which found that 30-50% of the 2026 data center pipeline may not materialize. We track large data centers and AI factories (>50MW) announced since 2024. A number of news outlets, including Bloomberg, Axios, and Semafor, picked up our research and spoke directly with our analysts, doing a great job at translating our findings for a broader audience.

From there the story spread like wildfire until the top trending topic on X was data center delays. However, as the broader ecosystem picked this up, the subtlety of our methodology was lost, quoting us as saying that half of announced datacenter capacity is likely to be canceled. Large accounts on social platforms oversimplified and went with the most eye-grabbing aspect of the story.

This led to some recent comments which also imply that we and others have relied on “vibe-coding” methods that focus primarily on announcements, which overestimate the amount of true developments in the pipeline that have a realistic prospect of coming to fruition.

We fully respect and appreciate the work of other analysts looking at this area and will always welcome a constructive exchange of views in what is a fast moving area. However, the statements made about our approach are incorrect and do not reflect what we believe or have said. As a result, we want to correct the record and explain what we actually do here at Currence.

Our objectives

Our journey towards analyzing data centers came via our background in energy research, which has always been at the core of our analysis. Although the general trend towards increased electrification was already underway, it has become clear that data centers are now the single most important driver. So we set out to track what was most important to us: a forward-looking view of the largest projects to understand the trends.

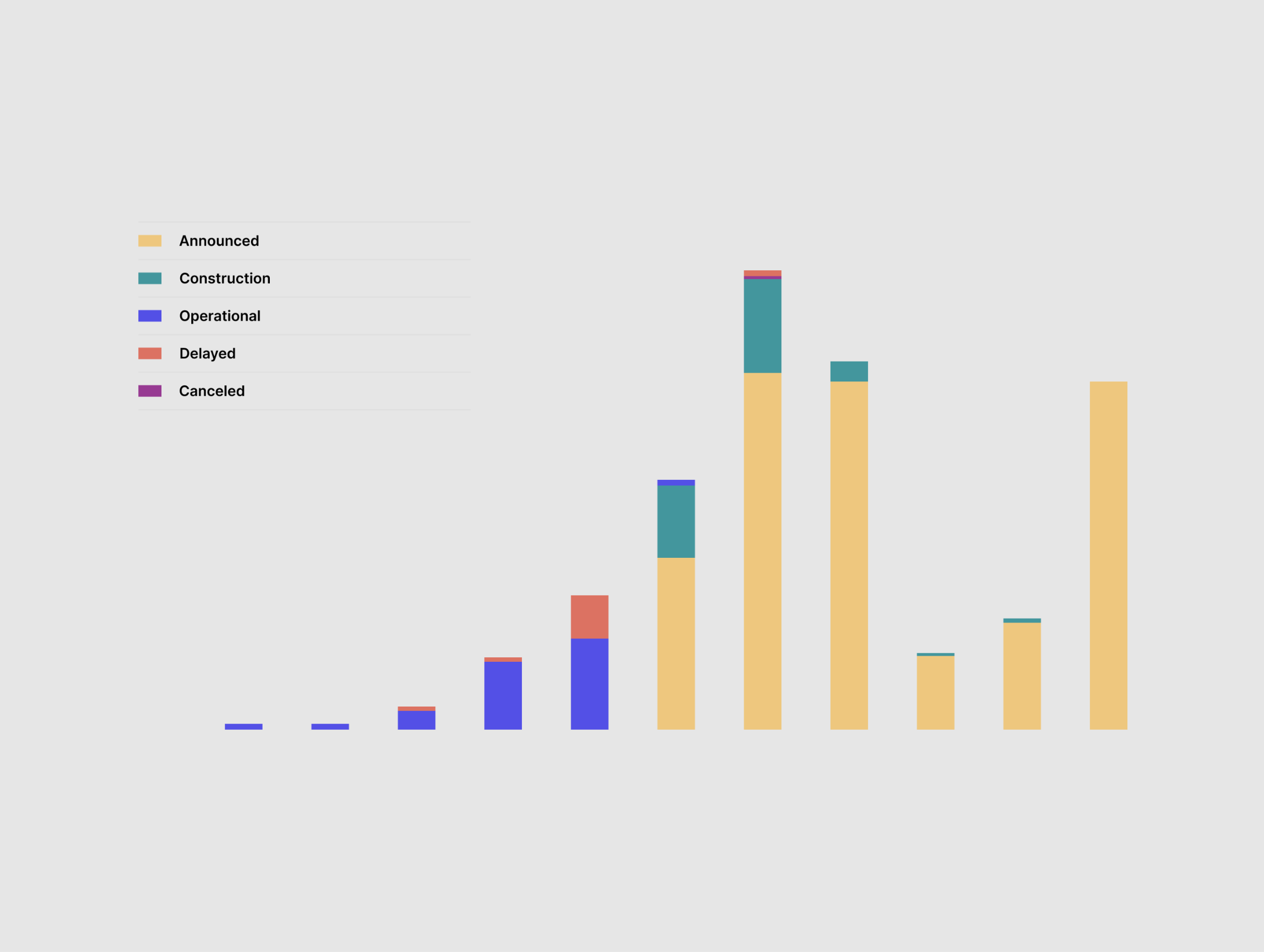

We track data centers that are >50MW in capacity and announced from 1 January 2024 onwards. This is not everything, clearly, and we emphasize this in the source line of every data center chart we publish. We do not track broad capacity goals, and we do not include information for which we cannot find a public source. We started with an intentionally narrow subject, to which we constantly add.

Our methodology

We track every relevant announcement — whether it be about plans for a datacenter, a grid connection, or deployment of onsite generation, energy storage or other electrical equipment. We record these announcements as they occur, for the year the developer stated it would come online. If a project is delayed relative to that original online date, we treat it as a delay and do not adjust the timeline to reduce that delay. We think this is a clearer, cleaner approach, although other analysts choose to dynamically adjust the target date. We do not add additional capacity that might be announced in future years. We then document and update projects as they shift their timelines later (or hit all their milestones).

We absolutely do not take such announcements at face value, as has been incorrectly implied. This is a pipeline, not a forecast, and we apply analysis and judgement to determine what is likely to happen. We are acutely aware that there are many speculative announcements that are unlikely to lead to capacity coming online as originally hoped for, if at all. We’ve often called them “paper projects,” and pointed out that the projects with serious backers and a solid supply chain are still likely to happen. We highlight why new projects entered our “delayed” status in our quarterly Outlooks, and explain whether it’s a signal for the industry or just a developer in distress. Power, contracts, and developer pedigree separate a credible project from a speculative one. Many projects are “low-information,” intentionally trying to attract some attention and get bought for the powered land.

We assess the prospects of these announcements through our credibility scores, including determining which projects are testing the waters and which ones have done the development legwork. We consider evidence from supply and offtake contracts, powering models, financing arrangements, time to power, and developer pedigree. We also continue to draw on our experience from similar analyses of project developments in geothermal, nuclear, carbon capture, and low-carbon fuels.

Our tools

As indicated above, we do not “vibe code.” That would certainly have been a lot easier. We use AI to ingest, enrich, and validate our data from thousands of sources including industry news, developer websites, permits, regulatory filings, financial filings, earnings transcripts, and more. Then we have experienced analysts who check our data and apply taxonomies, frameworks, and models. Our AI data engine was built by a world class engineering team and has developed novel methods for data enrichment and evaluation.

And finally…

Forecasts are great, and we all love to do them. However, they are only part of the story. They help to illustrate the scale of the problem in meeting the ever growing energy demands of AI. At Currence, we focus on the solution, in terms of what data centers and other players can bring to the table to help address the energy supply bottlenecks, including measures to contribute to grid flexibility and capacity, as well as helping to meet public concerns about any impact on energy prices or pollution. Our analysis draws on our underlying research into the economics, capabilities and deployment of grid technologies, short and long term storage, electricity generation and the power markets, all of which are fully available to our clients. We also profile specific examples of how these are being applied in the data center market to good effect.

The best market intelligence has always delivered trusted proprietary data, models to benchmark and forecast, and the point of view of expert analysts. AI doesn't replace that, it supercharges it. Currence combines the speed of AI with the trust of expert research.

Our market intelligence maps to how energy teams choose partners, forecast demand and price, and decide where to build, buy, or invest next. More than 90 teams already run on the Currence engine, including Microsoft, bp, Baker Hughes, Southern Company, HSBC, BBVA, Siemens Energy, Shell, BHP, B Capital, Galvanize, and Mitsui.

If you’re interested in learning more about our coverage, request a 20-minute call with our team.