We’re back after a quick summer break and easing into the post-Labor Day season with a look at what’s quietly working in clean firm power. Next-gen geo gets the hype, but an older plant just inked a major 25-year PPA, offering a preview of the future of power markets.

Old wells, new tricks

Last week, renewable energy developer Ormat Technologies announced it had signed a 52MW, 25-year extension of a power purchase agreement (PPA) for its Heber 1 geothermal project in southeast California. At a time when utilities are scrambling for clean firm power and headlines are dominated by next-gen geothermal breakthroughs, this agreement to give an old conventional geo plant a new lease — at a freshly negotiated price — is a slow-burn success now, but one that could shape how clean firm power gets built tomorrow.

What happened

Ormat, which develops vertically integrated geothermal projects, just scored a long-term, early renewal of its Heber 1 contract — notable for:

- The duration: 25 years is a long time in today’s power market.

- The offtakers: The Los Angeles Department of Water and Power (LADWP) and Imperial Irrigation District (IID) are both public agencies tasked with meeting California’s 2045 100% clean energy mandate.

- The technology: Heber 1 is conventional geothermal (aka, hydrothermal) — drilling into naturally occurring geothermal systems to tap steam, or in this case, hot water that is brought to the surface to run a turbine and generate power. It uses air-cooling, which is less efficient than water-cooled designs but more suitable for water-stressed regions like southern California. Ormat notes it’s using the latest air-cooled technology following a successful repowering of the plant.

The result: LADWP and IID lock in target-compliant, clean firm capacity at a time when every marginal megawatt is increasingly expensive and contested. And Ormat gets a guaranteed long-term return on a depreciated asset that now runs on mostly opex.

Why it matters

Conventional geothermal like Heber 1’s is reliable, mature, and often overlooked in favor of exciting EGS and closed-loop innovations. But it’s also already operating today. And at a moment when US electricity demand is climbing for the first time in decades, in a market where new capacity takes years to build, all while affordability pressures are mounting, that matters. See the chart below for the math:

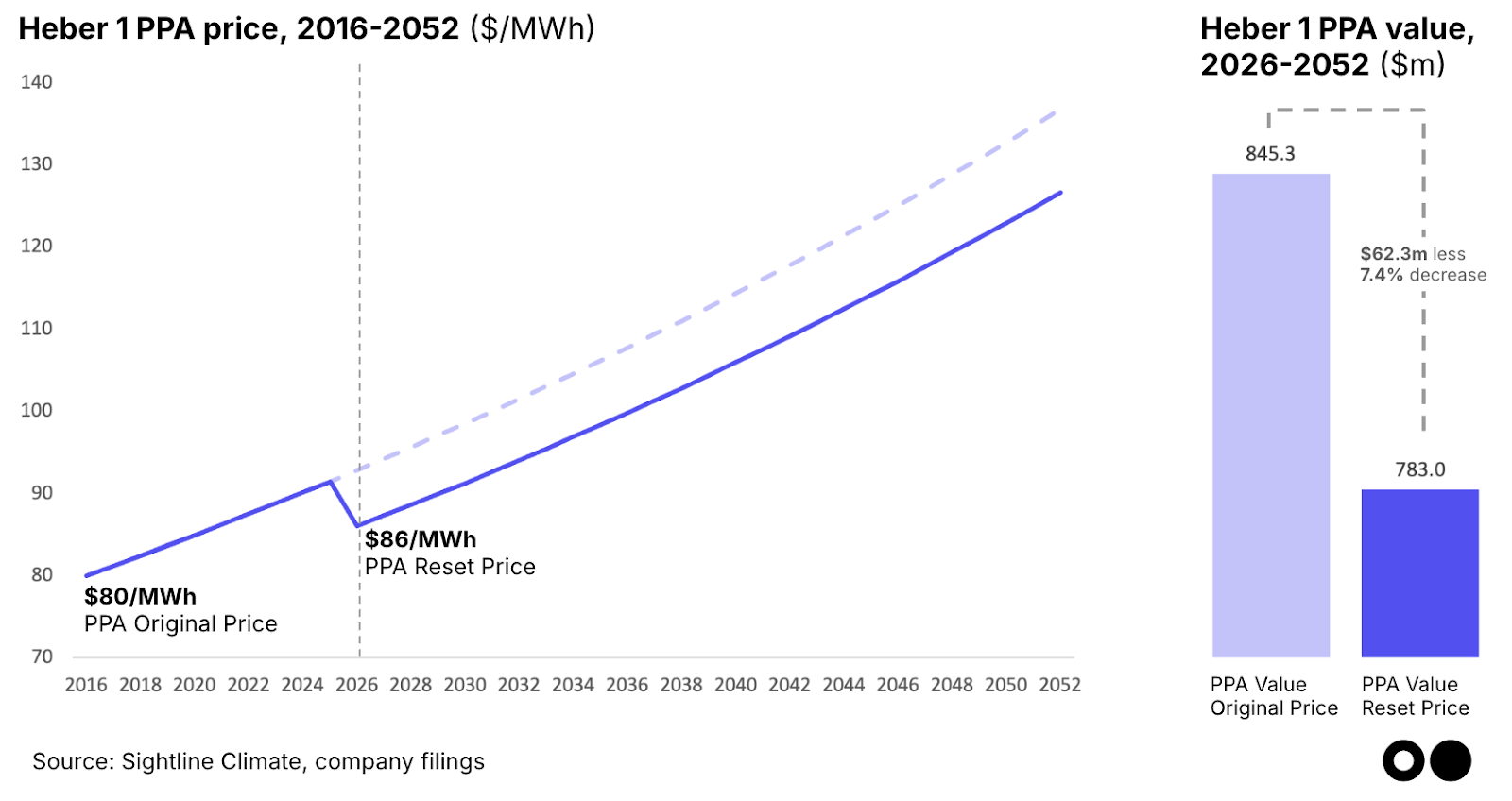

- The last Heber 1 PPA was for $80/MWh with a 1.5% annual escalator.

- The new contract starts at $86/MWh, keeping the same escalator — a higher starting price, but a discounted long-term value

- When you model it out, the new PPA yields a total contract value of $783m — a 7.4% decrease ($62.3m) from the trajectory of the old agreement.

It’s a win-win: Ormat locks in 25 years of cash flow from a fully operating plant, with operating costs likely to be well below the new PPA price. Meanwhile, LADWP and IID secure long-term clean firm power at a lower-than-market rate. Compare that to Fervo’s Corsac Station PPA with NV Energy, which is $107/MWh for 15 years.

That’s not to discount next-gen geothermal. The tech is quickly becoming a favorite for meeting surging demand from data centers and other large loads, and leader Fervo is posting blockbuster results left and right, proving out the potential of enhanced geothermal. But in today’s power markets, greenfield challenges persist: long development timelines, financing gaps, and clogged interconnection queues. Which is why the near-term opportunity may lie in getting “back to the future” — deploying next-gen techniques at existing geothermal fields. By re-drilling, applying novel EGS stimulation, or even using AI to re-map known resources, developers can unlock stranded capacity at lower risk, shorter timelines, and cheaper cost.

Take startup Zanskar, which acquired the underperforming Lightning Dock in New Mexico in 2024. Zanskar’s AI platform GeoCore identified a hotter, higher-permeability zone near the original wells. By re-drilling directionally from the existing pad — avoiding costly new surface work — the team slashed development costs by 75%. Within 12 months, Lightning Dock jumped from 4–7MW to its full 15MW capacity, what Zanskar says is the most productive pumped geothermal well in the US.

Meanwhile, geothermal developer Greenfire Energy is working with power generator Calpine at the geothermal site, The Geysers in California, to apply closed-loop retrofits, while Ormat also announced a partnership with Sage Geosystems to pilot stimulation tech at existing wells last week. (Meta already tagged Sage for geothermal for its data centers last year.)

Key takeaways

- Uprating joins the party. Geothermal’s fastest megawatts may not come from wildcatting new fields but from squeezing more out of existing ones. AI, novel stimulation, and better drilling techniques are already unlocking more capacity. Because subsurface conditions are known, uprates often avoid new water rights, land-use battles, or surface equipment, making them faster and less risky.

- It’s all about the marginal megawatt. In a market with rising costs and political headwinds, every extra MW of clean firm power matters. For utilities and hyperscalers chasing 24/7 carbon-free capacity, uprates deliver speed and predictability, often at prices below greenfield projects. Consider: the Heber 1 PPA doesn’t cross Fervo’s Corsac Station price until 2041.

- Time to make some calls? There was a flurry of development in conventional geothermal across the western US in 2008-2012. Most of those facilities were on 15- to 20-year PPAs, and will be coming up to their expiration dates in the next few years. Some of those assets might be on the table for uprates, repowering, or re-contracting, like Heber 1.

Clients can get geothermal project data and commentary here, and dive deeper into geothermal's economics and innovations. If you’re interested in becoming a client, talk to our team.