The DOE just pulled $3.7bn from 24 major clean energy projects — a reversal that threatens the US' industrial decarbonization. Here’s what got cut, and why it matters.

FOAK funding fallout

Last Friday, in a late-afternoon news dump, the Department of Energy announced it is canceling $3.7bn in funding across 24 clean energy projects. It’s the most sweeping climate funding rollback yet under the Trump administration — and a direct hit to the Office of Clean Energy Demonstrations (OCED), the federal office created to commercialize first-of-a-kind (FOAK) decarbonization technologies.

What happened

Led by newly appointed DOE Secretary Chris Wright, the department recently launched a sweeping review of $15bn in awards across 179 projects. Now the results are in: 24 OCED projects have been terminated, cutting across nearly every corner of industrial decarbonization — low-carbon cement, carbon capture, hydrogen, clean fuels, electrified heat, and materials like glass and steel.

Wright framed the cancellations as a cost-saving measure, claiming the projects “failed to advance the energy needs of the American people” and wouldn’t deliver “a positive return on investment.” Nearly 70% of the canceled awards, he said, were issued during the final weeks of the Biden administration.

But these weren’t fringe initiatives. OCED, launched in 2021 and backed by more than $25bn from the Bipartisan Infrastructure Law and Inflation Reduction Act, was designed to bridge the commercialization gap, supporting diligenced projects with proven technologies and unproven markets. The office offered non-dilutive, cost-share awards (up to 50% of capex), with funds released in tranches tied to development milestones. Many of the projects had not yet drawn down their full awards.

Among the hardest-hit sectors:

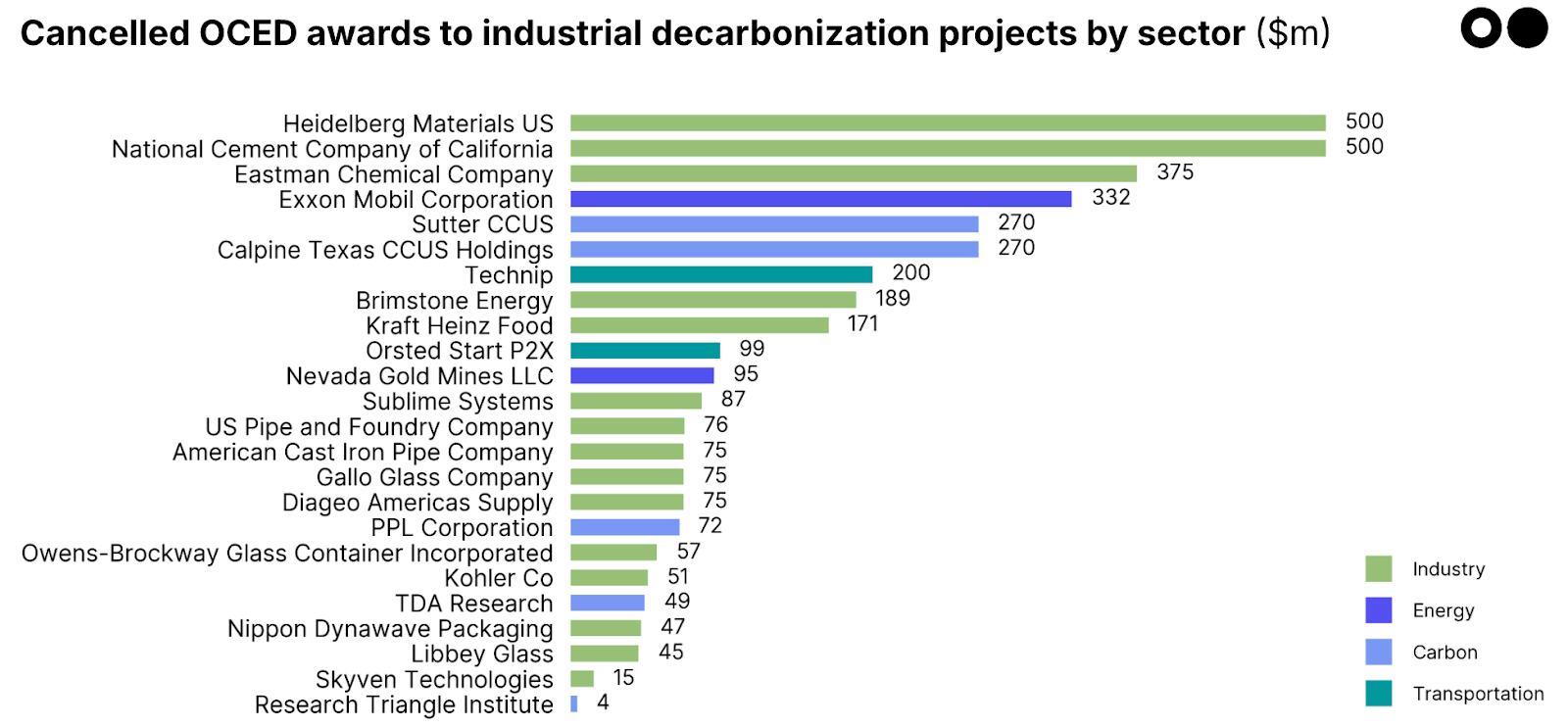

- $1.3bn in low-carbon cement (Brimstone Energy, Heidelberg Materials, Sublime Systems, National Cement Company)

- $665m in carbon capture/CCS (Sutter CCUS, Calpine Texas, TDA Research, PPL Corporation, Research Triangle Institute)

- $631m in hydrogen and low-carbon fuels (Exxon Mobil, Orsted Start P2X, Technip)

- $375m in chemical recycling (Eastman Chemical Company)

- $359m in clean heat and electrification (Kraft Heinz, Kohler Co, Diageo, Skyven Technologies, Nippon Dynawave Packaging)

- $177m in low-carbon glass (Gallo Glass, Libbey Glass, Owens-Brockway)

- $151m in low-carbon steel (American Cast Iron Pipe Company, US Pipe and Foundry Company)

- $95m in solar (Nevada Gold Mines)

Sightline clients can explore clean industrial project deployment charts on our platform here. If you’re interested in becoming a client, speak with us here.

Why it matters

OCED was one of the most ambitious tools the federal government had for scaling climate infrastructure. Its model was to de-risk market adoption, not technology development — helping FOAK projects attract follow-on capital and reach liftoff. Many canceled projects had signed offtake agreements, EPC contracts, and local partnerships in place. Several were already breaking ground, and notably, many were located in red-state manufacturing hubs, promising to deliver jobs and economic benefits to disadvantaged communities.

Cement has been hit hardest: including projects not finalized, the total public support now pulled from the sector stands at $1.5bn (including not-awarded funds), or 94% of federal funds earmarked for low-carbon cement under the Industrial Demonstrations Program. These projects represented nearly 60% of planned low-carbon cement capacity in the US.

This is a major setback for industrial decarbonization, at a time when the Trump administration says it wants to strengthen US manufacturing competitiveness (👀 tariffs). Sectors like cement, CCS, hydrogen, and clean heat, all facing offtake and cost hurdles, just saw their commercialization timelines stretched — or erased entirely.

Additionally, according to the Center for Climate and Energy Solutions, the cancellations could result in 25,000 lost jobs and $4.6bn in lost economic output.

What’s next

- Without federal cost-share, these FOAKs will need to (and possibly struggle to) raise alternative capital. The OCED cancellations sent a clear message: even awarded federal funding isn’t safe. The Loans Programs Office also canceled a partial load of nearly $3bn to residential solar installer Sunnova last week. Now, developers must now lean harder on expensive private sources — venture equity, project finance, or strategic capital — to move forward. Startups may seek new homes in Canada or the EU, where industrial decarbonization support remains intact, but it won’t be easy.

- A lost competitive edge in low-carbon materials production. The combination of OCED grants and tax credits was set to make the US the cheapest place in the world to produce low-carbon materials. It had already drawn new investment commitments in reindustrialization and the promise of more in supporting infrastructure like hydrogen and electrification. Withdrawing this funding will hand that advantage to Europe or China, and leave areas that lost uneconomic fossil industries without a replacement.

- Still, projects just got easier in one regard: permitting. Last week, the Supreme Court handed developers a win by narrowing the scope of NEPA reviews. In a unanimous ruling, the Court said agencies don’t have to evaluate upstream or downstream environmental impacts beyond their jurisdiction — streamlining timelines for energy, transportation, and industrial projects. A win for speed, even as funding falters.