The LinkedIn-o-verse lit up this week with geothermal news, from the 31MW PPA signed between Fervo and Shell Energy to the 10MW PPA between Baseload Capital and Google. These are huge, but there was another market signal this week that went a bit under the radar — the Utah BLM geothermal lease sale.

On 8 April, the Utah division of the US Bureau of Land Management (BLM) held a geothermal lease sale. It netted a total $5,768,084 across 14 leases, from five different winning bidders. There was a fair bit of excitement in the geothermal community about a 3,934-acre (1,592-hectare) parcel that an LLC called Buffalo River Minerals paid $344/acre for, or just over $1.3m. This parcel, along with the other high-bid ones, are just down the road from Fervo’s Cape Station site, which Fervo got for mere dollars per acre back in 2018–2021.

I’ve been closely watching lease sales since 2008, as they are ridiculously interesting indicators for sector interest. They tell us about demand, players, and how the project pipeline could look in years to come. The high bid this time was nowhere near the all-time per-acre bid, set by Ormat in 2009 for $3800/acre for a parcel in Nevada, but it’s way up from where it was in recent years.

And importantly, these lease sales are a signal. Sightline looks at sector readiness across seven categories (see below) and monitors signals to determine whether things are on an up or downward trend — something we’re currently building products around, so please ask us about it!

But what can these signals tell us about next-gen geo sector readiness – especially in the context of meeting growing demand for clean firm power?

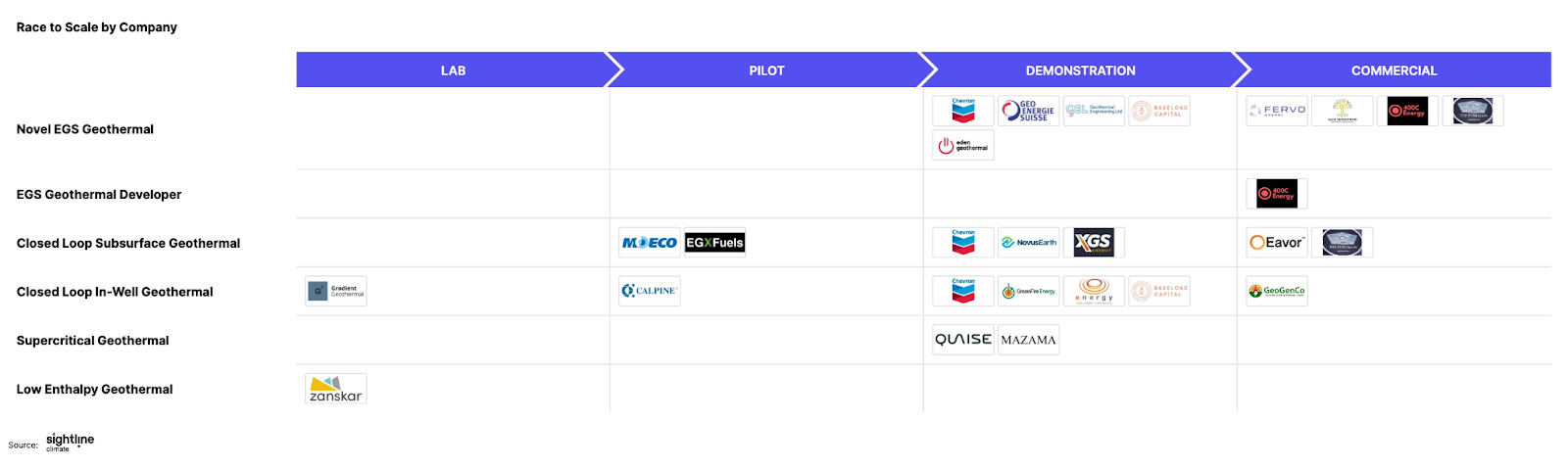

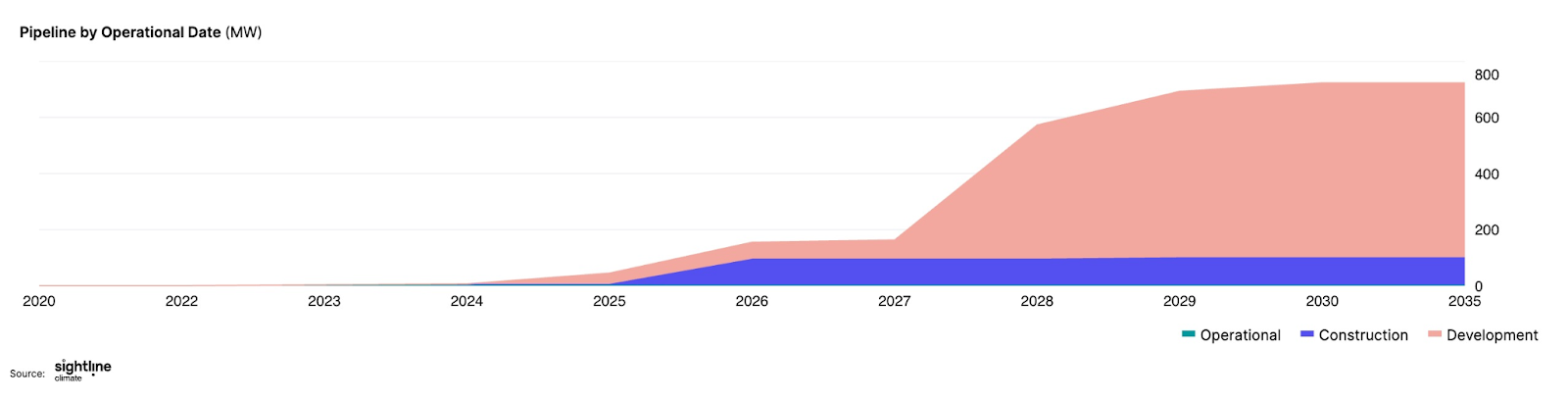

1. Deployment is moving, but flowing electrons is the only thing that matters. The lease sale and other announcements we’re hearing are positive signs, but see the chart below for the back-to-reality take. In next-gen geothermal, only 3.5MW or 0.4% of planned capacity is online — 86% has not yet reached drilling.

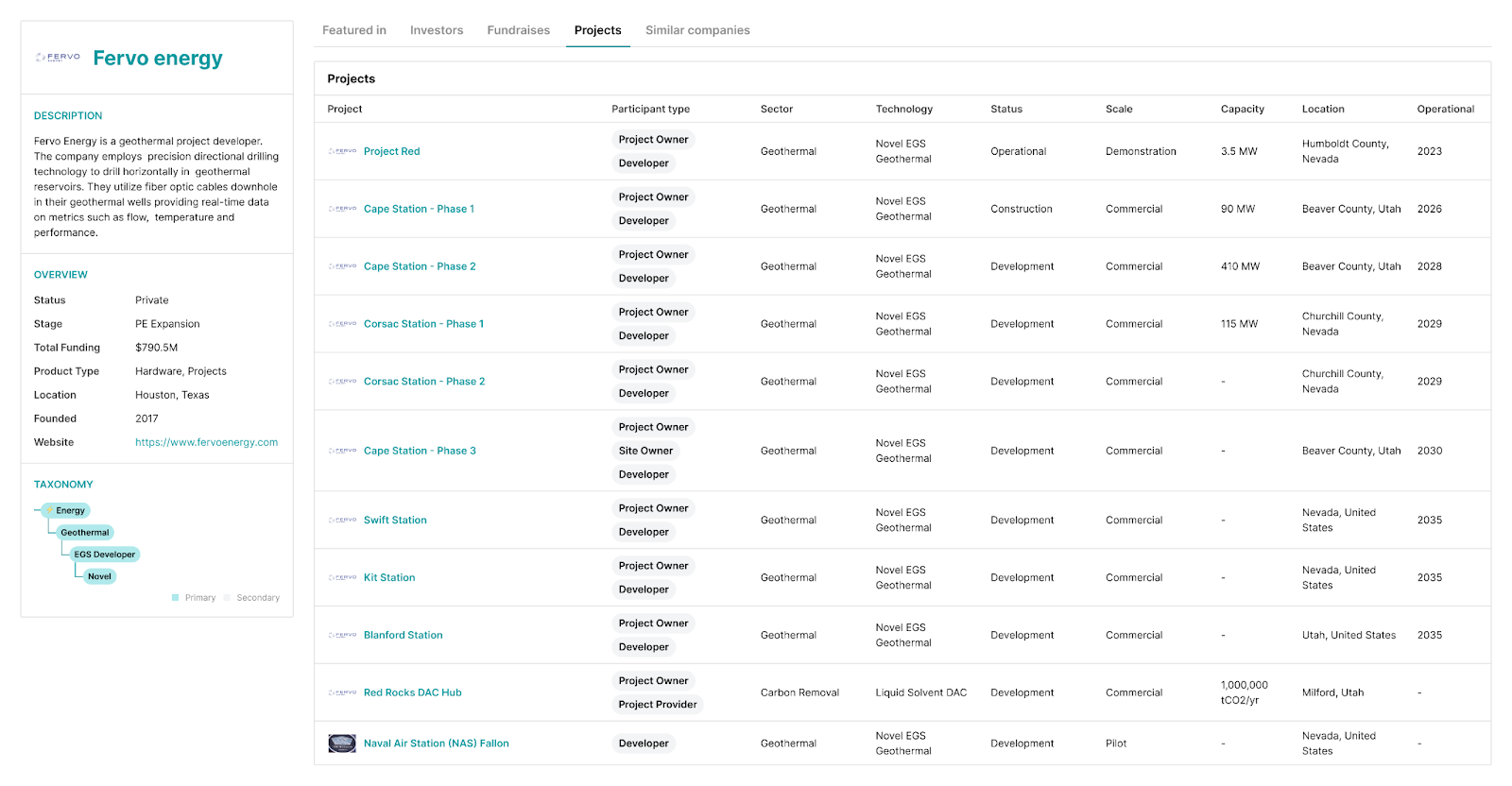

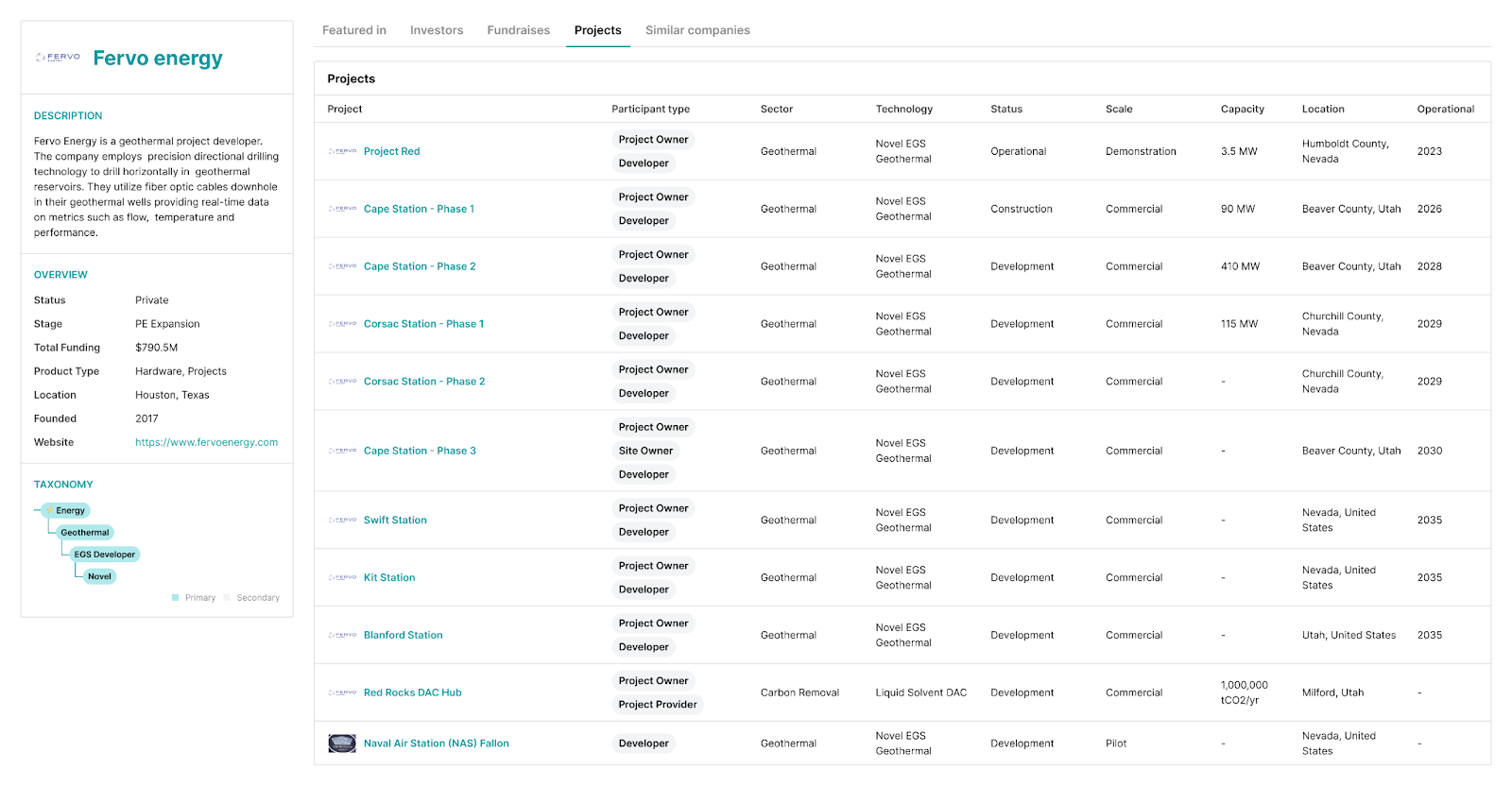

2. Demand is there, with upside for the quick. In the PPA with Baseload Capital, Google stated that the power — set to come online in 2029 in Taiwan — is bookmarked for data center operations. Demand is there for US players as well, as hyperscalers and power retailers try their best to not have to choose between cost, sustainability, and reliability — the idea is that geothermal can provide all three. In fact, Fervo upsized its Cape Station project from 400MW to 500MW to accommodate the Shell Energy PPA. Fervo has other projects in earlier development stages, but presumably the parties agreed that time was of the essence and chose to expand Cape rather than get an agreement for a project due online later (Fervo project portfolio here. Read about the Cape Station in our case study here.

3. Players are diversifying, no longer a VC-only game. It makes sense that Fervo was VC-funded — it was trying something new and different. But now that founders Tim and Jack have seem to have cut a path forward, the next announcements might not be from the startup world.

Why do we think this? Take the Utah lease sale, and stay with me on this one: In the olden days, I could relatively easily trace the bidder’s dummy LLC back to who actually made the bid, most often by using the registered address. This would take me to an actual business address, or in some cases, the home address of the bidder. But the geothermal sale bidders are getting more sophisticated. The overall sale winner, Buffalo River Minerals LLC, is all but untraceable — which is decently common in oil & gas for bidders to maintain secrecy or competitive advantage. And Percheron LLC is a fairly well known service provider that specializes in securing land and mineral rights on behalf of bigger players. While not readily quantifiable, that the bidders are sophisticating is itself a signal.

Now, what does that mean for actual development — could 2025 be the year of some blockbuster moves? Majors like Chevron have projects of their own and are investors in companies like Baseload. Services providers like Baker Hughes, Helmerich & Payne, and others are hedged across closed loop, next-gen EGS, and even super-deep geothermal. Everyone seems poised to make a move. A couple years ago, we were saying it was all eyes on Fervo to get to first power at Cape for others to get in the game, but we suspect it’ll be a lot sooner than that.

Bonus: It looks like EGS is pulling ahead. The signals this week are centered on Novel EGS. Yes, there are closed-loop developments out there, the largest of which is Eavor’s Geretsried project — notably, the offtake agreement there is for heat, not power. Right now, electrons are king, and if Novel EGS is the one that proves it can deliver, and reasonably soon, it’ll be the winner.