It’s a clean energy golden rule that a path to cost parity unlocks emerging tech. Whether solar, wind, EVs, or lithium-ion storage, it’s been the same play: pathway to a competitive cost (even if supported by policy) → deployment takes off → further cost declines → exponential deployment.

But to see if the technology can get to competitiveness, you need benchmarks.

As we've been building out our projects database and the case studies you've seen, we've also been gathering comprehensive benchmarks on cost and performance.

Here, we’ll take a closer look at LDES, or what we define as >8hrs storage. Our sector analyst Lukas pulled together an initial look at the numbers for this sector in his latest Sightline, Benchmarking shows few LDES techs are competitive with lithium-ion.

LDES is still pretty early days as a sector, but the first-cut benchmarks already tell us a lot.

1. Few LDES techs are anywhere near competitive with lithium-ion yet.

Despite the theoretical advantages emerging LDES techs have – cheap raw materials, onshored supply chains, or “decoupled power and energy” – costs are often much higher than the quick-and-dirty fix of simply derating a 4-hour lithium-ion BESS to have lower power output (aka long duration lithium-ion).

So the reality is, LDES techs are more expensive than long-duration lithium-ion batteries, which itself is rarely profitable above 4 hours without policy support.

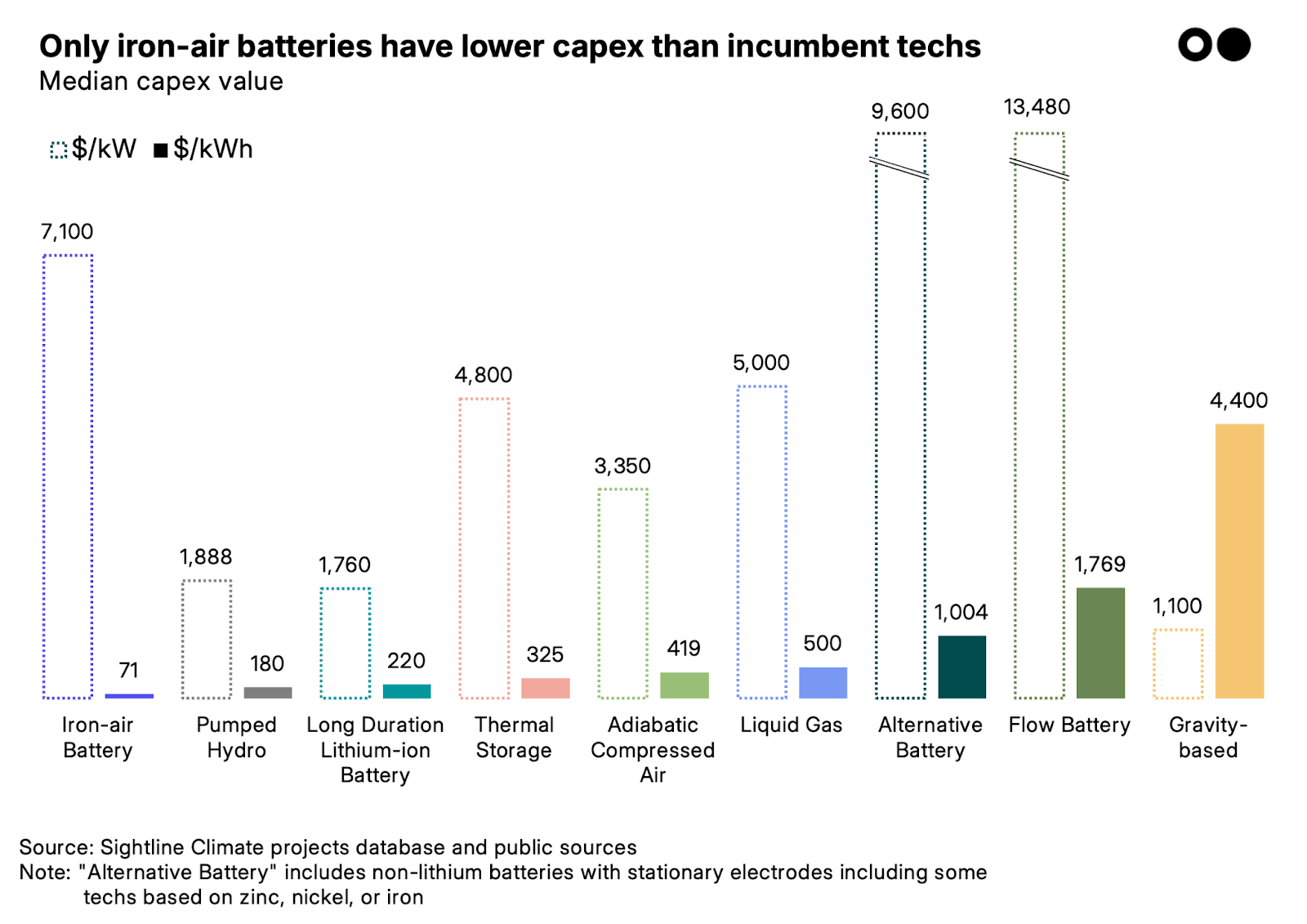

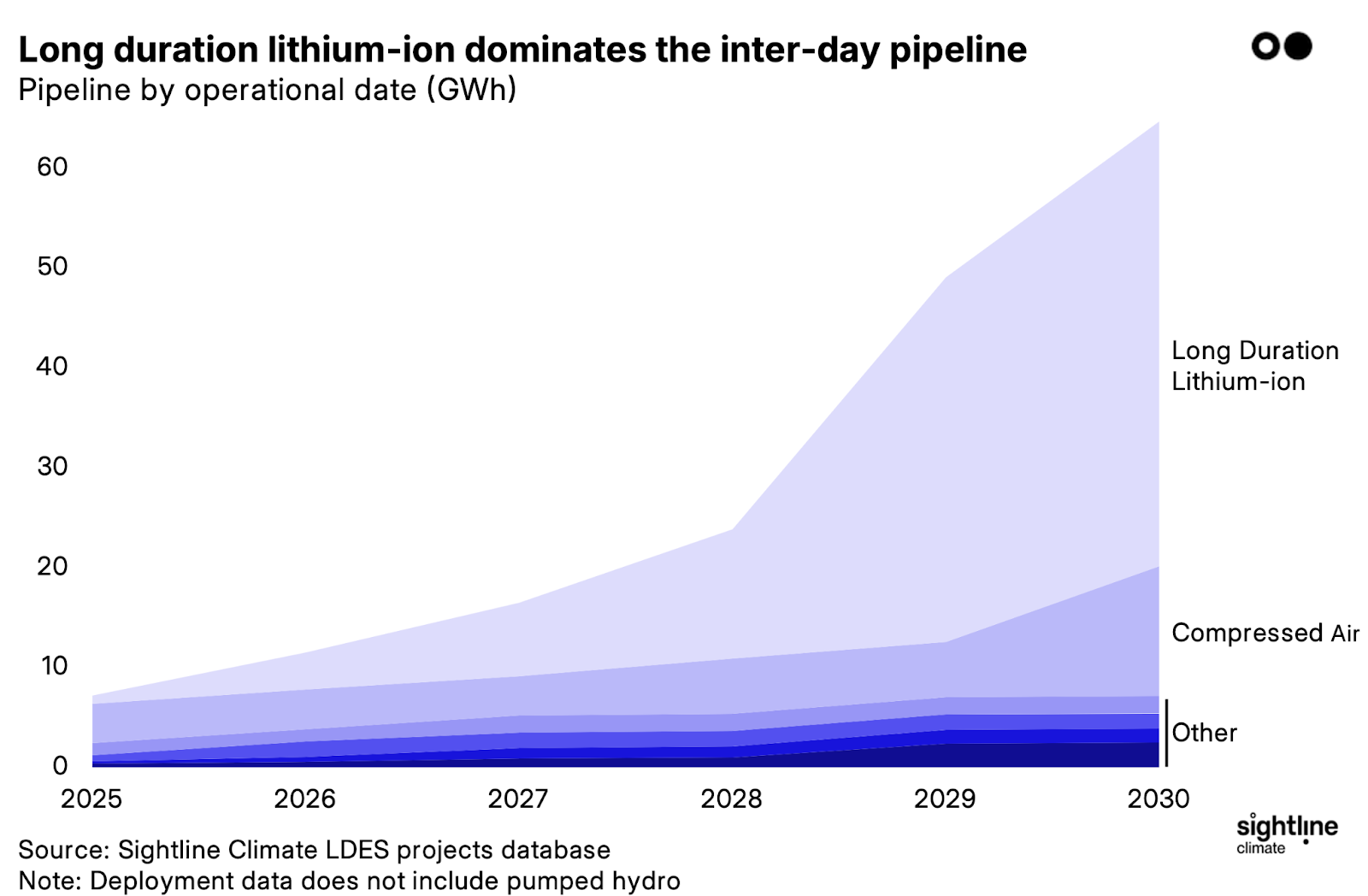

Almost everything is at least 50% more expensive than lithium-ion – except for Form Energy’s iron-air tech (which might be priced below cost 👀). The chart shows project capex ($) divided by capacity (kWh) to give a quick sense of upfront costs. The outlined bars show what this is in $/kW terms – the longer the duration of the system, the more kWh per kW, and the higher $/kW costs are.

This shouldn’t really be a surprise given that no company has built two commercial projects, let alone the dozens of projects that bring techs down a cost curve. But it’s striking just how far behind some emerging techs are. Flow batteries (tech profile), the classic LDES tech? Seven times as expensive as lithium-ion.

How about the low-capex, high-opex play of thermal storage (tech profile)? 50% more expensive upfront than lithium-ion, even before considering the charging costs.

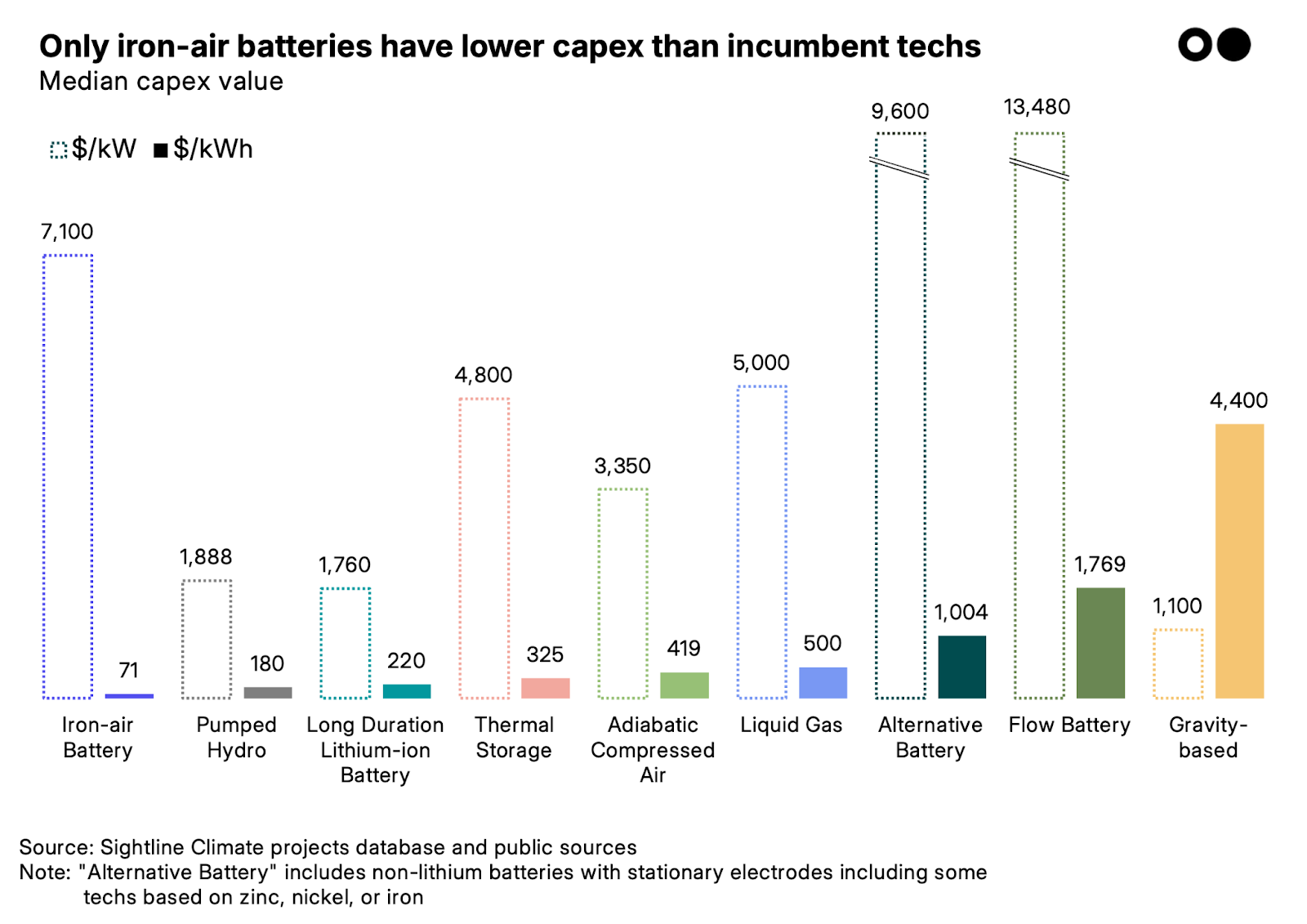

2. Lithium-ion’s cost advantage already shows up in the deployment data.

See the chart below, built from our LDES deployment data (soon to be released on our projects dashboard) – 37% of the 2030 LDES project pipeline is long duration lithium-ion. Its main competitor is compressed air (54%), but those deployment figures are inflated by two green hydrogen-fueled diabatic compressed air projects in Germany, 26.9GWh each (!!), whose developer Corre Energy hasn’t made meaningful progress towards FID and was delisted this March. Exclude these two projects, and lithium-ion’s share jumps to 64% – twice every other tech, combined. Whenever governments stand up LDES subsidies (e.g. Australia, California, UK, etc.), long duration lithium-ion fills the void left by emerging techs that are too expensive and/or too immature.

Don’t just take my word for it, in 2024 the California Public Utilities Commission stated that, other than lithium-ion, “No other LDES alternatives have been identified by [load-serving entities] to meet the 1000MW obligation” under California’s Mid-Term Reliability standard.

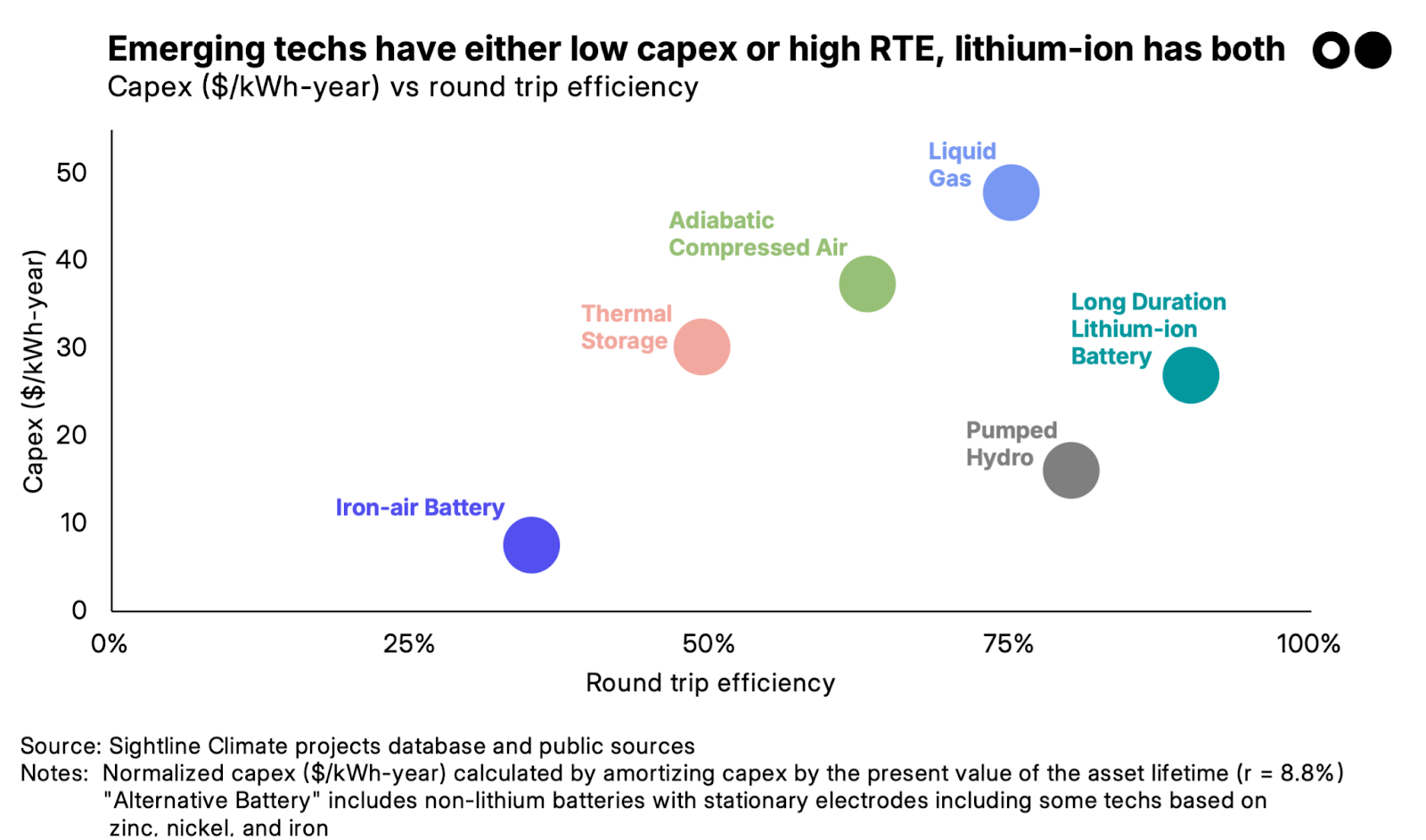

3. Capex makes it clear. Even though most LDES techs are quite expensive on the whole, there are a few individual companies that are clear leaders in the crowded field. And most of that boils down to asset lifetime. The comparison above wasn’t quite fair because techs like liquid CO2 can last for 30+ years, while lithium-ion needs replacing after 15. Take lifetime into account (for the spreadsheeters out there, we divide capex by the present value of the asset lifetime, r = 8.8%) and 🥁… most LDES techs still have higher capex than lithium-ion (see below).

We've taken this measure of capex ($/kWh-year) and combined it with round trip efficiency, a good proxy for charging costs, the main opex component. Low and to the right is where you want to be, but emerging tech is finding itself high and to the left.

Some bright spots, as it turns out: Energy Dome’s FOAK is just 30% more expensive than lithium, while Echogen’s pumped thermal storage project in Alaska is actually cheaper upfront. Of course, this doesn’t solve the problem that these techs all have lower round trip efficiency and therefore higher charging costs than lithium-ion, as you see in the chart above.

So, there are a few notable exceptions, but long duration lithium-ion is the tech to beat in LDES. But betting against lithium-ion usually doesn’t end well.