Last week, on 21 May, the EU officially adopted new regulation aimed at kicking up its nascent carbon capture and storage (CCS) capacity. Under the Net-Zero Industry Act, the bloc must develop at least 50 MtCO2/yr injection capacity by 2030, and 280 MtCO2/yr by 2040. And, in a bold move, it makes major oil and gas players in Europe foot their proportionate share of the bill.

Call me a jaded energy analyst, but my immediate reaction was, it won’t work. It wouldn’t be so hard to imagine that companies would simply pick up and walk away from EU oil & gas production. Most have higher-production assets elsewhere, and with oil prices hovering around $65/bbl right now, it would seem to make economic sense. Just look at Exxon and Shell, who exited the North Sea last year after 60 years producing there.

But the EU did a couple of things that were quite clever. For one, companies’ obligations are tied to past production, from 2020–2023, not ongoing or future production. Any firm that produced enough during that window is on the hook — the regulation names 44 companies that together accounted for 95% of the EU’s oil & gas production in that time. Even if they divest or shut down operations today, they’re still responsible for contributing to the collective 2030 target.

So by the end of 2030, each obligated company must demonstrate operational storage capacity in geological sites certified under the CCS Directive. These sites will be made available to CO2 emitters, particularly from hard-to-abate sectors, effectively forming the backbone of Europe’s future CO2 value chain. They’ll be designated as “Net-Zero Strategic Projects,” unlocking potential advantages in permitting and access to funding.

Enforcement mechanisms have yet to be defined in detail, but if the precedent set by other EU net-zero rules holds, consequences could include reduced access to future permits, funding, or public contracts. That said, enforcement is likely to vary across member states.

There’s lots here that’s interesting, but here’s what especially caught our eye.

1. A new kind of SaaS: Storage as a Service?

Right now, the regulation is in the standard EU “scrutiny” period, so we’ll find out more over the next month or so. But 30 June is when obligated entities are required to submit plans for how they are going to contribute to the Union target, including project milestones and the pathway to meeting assigned volumes.

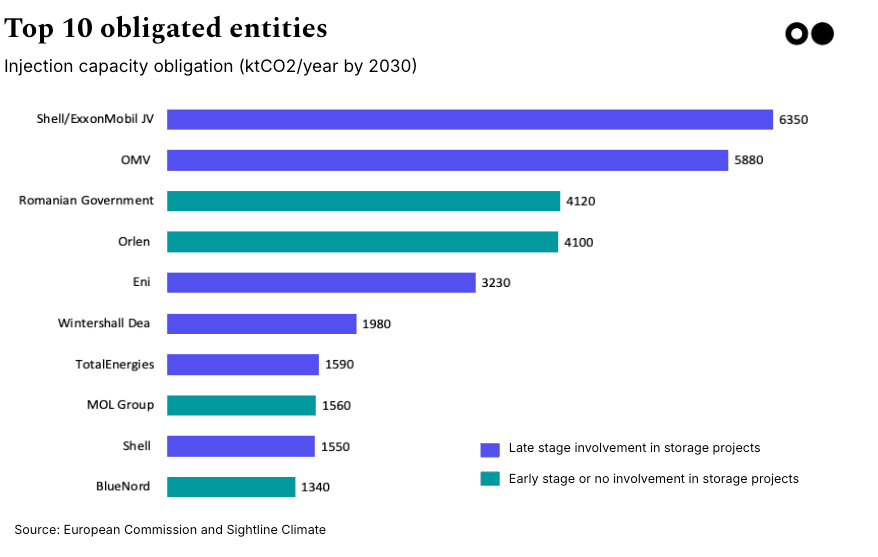

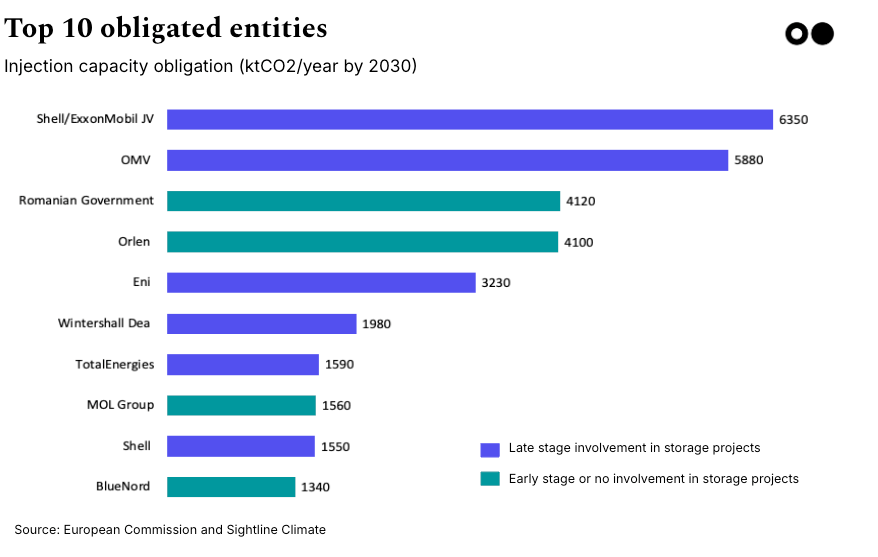

Most of the biggest emitters are already involved in storage projects. But they’ll likely have to expand them, or build more. The top five contributors together (see below) are responsible for over 26% of the total obligation. Nederlandse Aardolie Maatschappij (NAM) alone — a Shell/ExxonMobil JV — must deliver 6.35 MtCO2 of injection capacity annually.

But can they do it at a profit? And can they do it in such a way that the transport and storage part of CCS is largely taken care of, so point-source emitters (or put differently, project developers or CO2 suppliers) can consider that part of the value chain as de–risked, thereby reducing project uncertainty and cost?

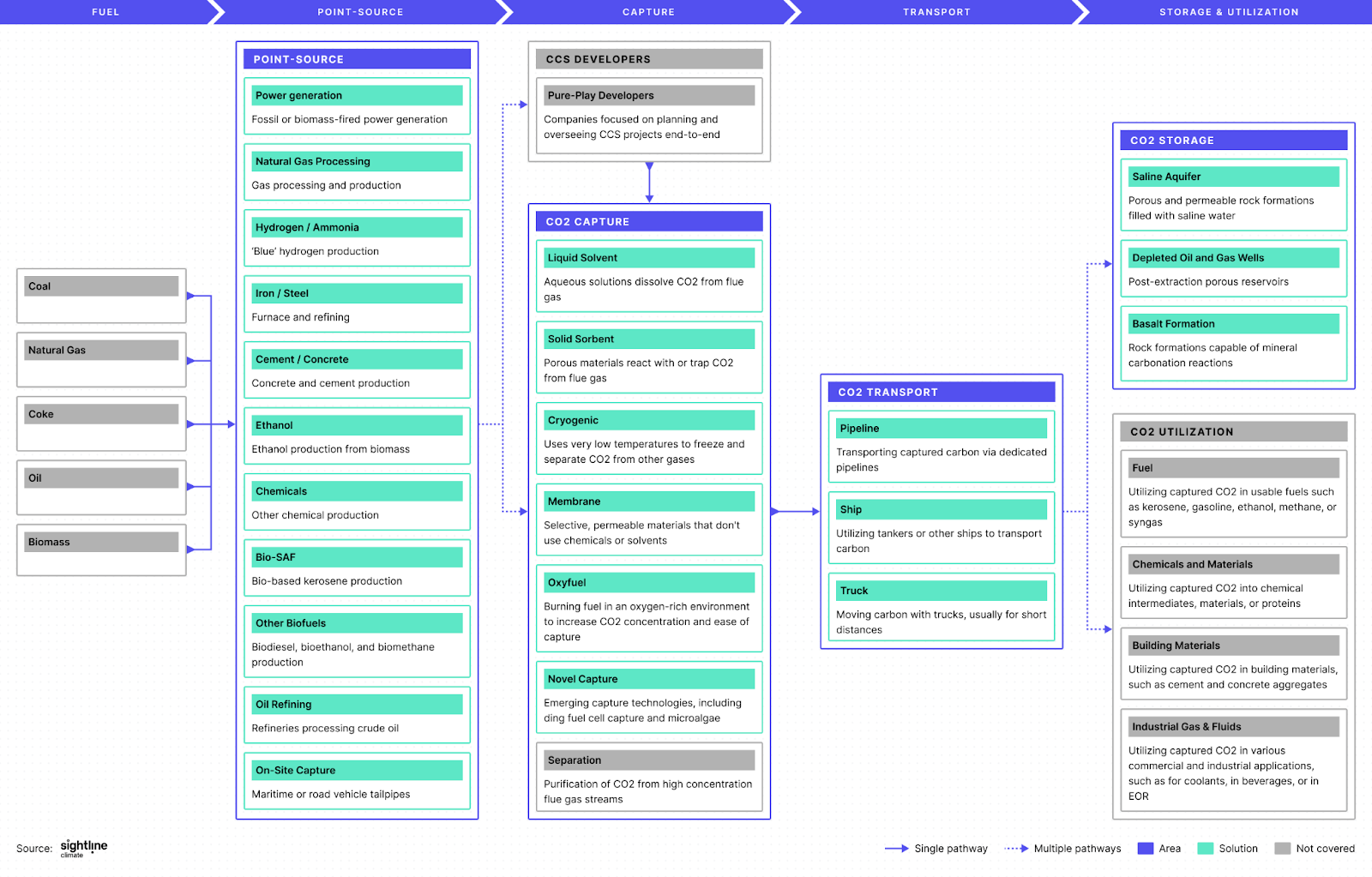

2. The CO2 has to come from somewhere.

The EU regulation mandates storage, not capture — meaning obligated companies are not necessarily required to capture CO2 from their own operations, only to ensure that storage capacity is available and operational by 2030.

But in 2030, there will be far more players capturing that CO2, with free allowances in the EU Emissions Trading Scheme (EU-ETS) ratcheting down, nudging sectors like cement, steel, and chemicals pretty strongly toward CCS.

In this scenario, CO2 becomes a commodity, like other industrial byproducts (used cooking oil --> SAFs, anyone?). The oil and gas producers, then, are already dealing with CO2 in their operations and have the technical know-how, geological data, and infrastructure to store it underground. They could bet on becoming providers of CO2 storage services for the wider economy and partners for smaller industrial emitters who pay them for access for storage capacity.

3. Why go alone if you can partner?

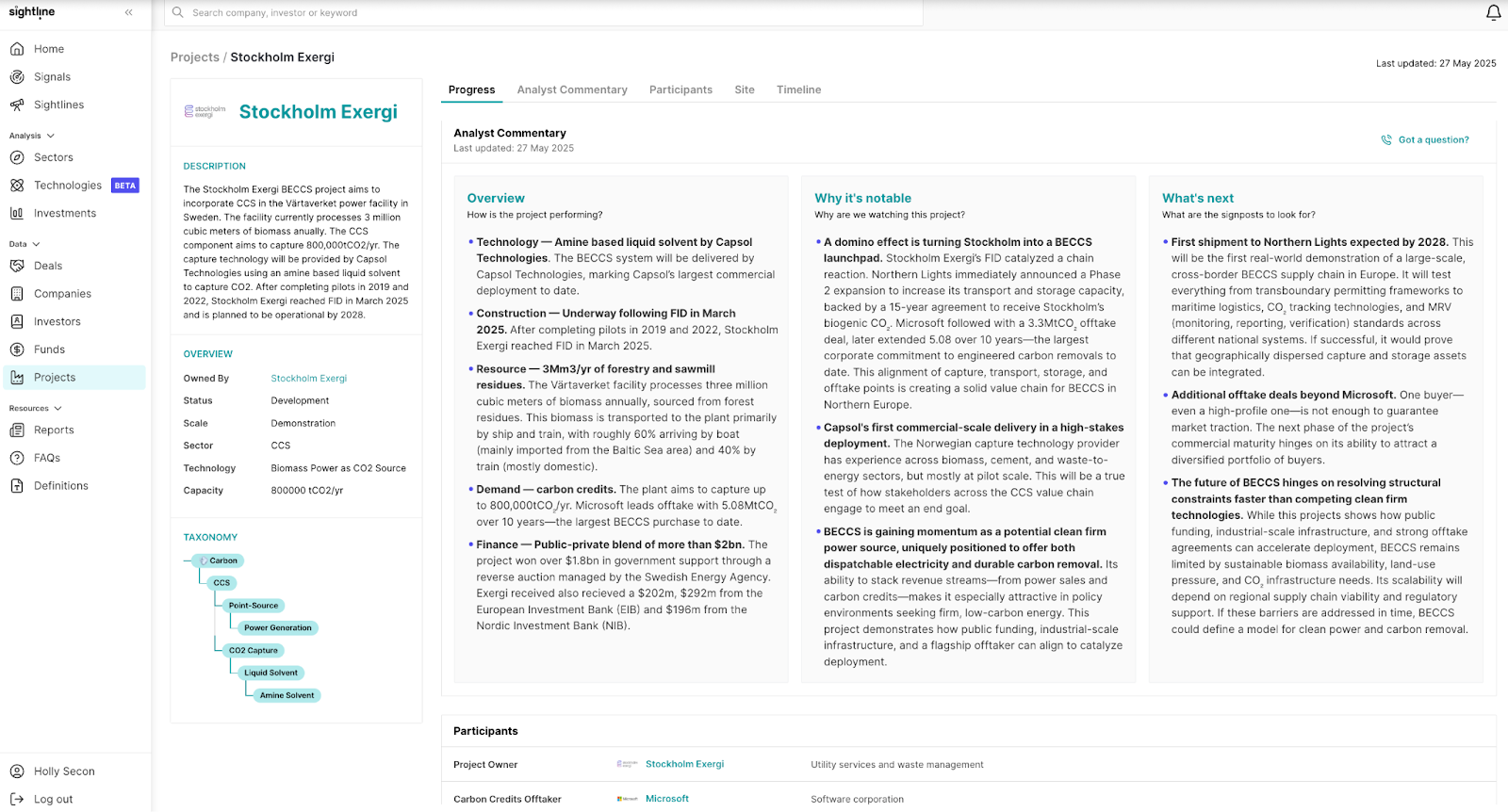

Rather than flying solo, obligated companies can meet targets through joint ventures or partnerships, and many already are. Shell, TotalEnergies, and Wintershall Dea are involved in some of Europe’s flagship storage projects today — Northern Lights (Norway), Project Greensand (Denmark), and Porthos (Netherlands). Together they could provide about 15.5MtCO2/yr by 2030 — 31% of the EU’s mandated capacity. The most advanced, Northern Lights, became operational in late 2024 and is scaling from 1.5Mt to 5MtCO2/yr by 2028. Critically, it has locked in firm offtake contracts with Stockholm Exergi’s BECCS facility — backed by SEK 20 billion in public funding and set to export up to 8kt of biogenic CO2 annually — and with Ørsted’s Kalundborg BECCS project, which secured long-term injection rights and became the first Danish project with full-chain removals via maritime CO2 export in Europe.

These are real, operating storage projects — proof that much of the needed infrastructure is already under construction or could be co-developed by existing players. With ETS tightening, ETS2 on the horizon, waste-to-energy entering the fold by 2028, and BECCS and DAC gaining traction, storage demand is set to surge. Now, supply can step up and meet it.