.png)

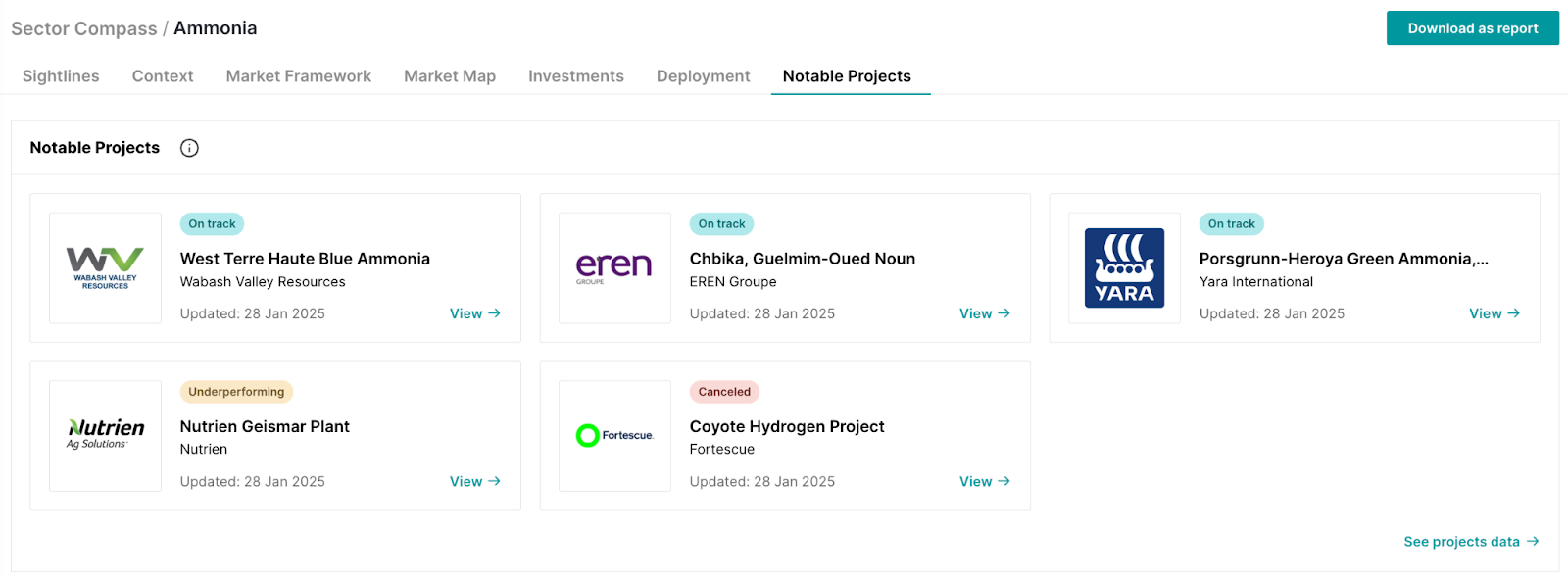

If it’s not been apparent, we’ve been following the IMO’s new Net-Zero Framework announcement pretty closely — we covered it in this week’s CTVC newsletter and published client-exclusive commentary on it. TLDR? The IMO set the roadmap for its planned 30-43% reduction in the greenhouse gas fuel intensity (GFI) of ships by 2035 (and higher beyond that), including introducing the first global carbon tax, with real penalties for non-compliance, and trading or banking for those exceeding targets. Clients can read our full take here, and explore competing maritime decarbonization solutions in our Maritime sector compass, Ammonia coverage, and Ammonia notable projects.

But this got us thinking — what’s going on in other carbon arenas like the EU Emissions Trading Scheme (EU-ETS) or CBAM right now? Currently, it covers industries like power production, energy-intensive sectors (such as oil refineries, steel, cement, aluminum, glass, and pulp and paper production), as well as intra-EEA aviation and maritime shipping. Numbers just got released on the state of the market in 2024, which we also covered in a recent Sightline: Global carbon price revenues fall for the first time in a decade. (Spoiler: The EU-ETS seems to be in a bit of a doldrums.)

But things could change as the EU Commission is gearing up for a bigtime review of the ETS in 2026, to evaluate ahead of plans to expand to more sectors in 2027. In the run-up, the Commission launched a call for public consultation just last week. Here we’ll look at some of the proposed changes and what they could mean for the market.

1. Tighten the cap or lower the floor — diametrically opposed.

The Commission sets the cap and floor for the ETS, and it’s getting pushed in two very different directions. One is to tighten the cap (helping meet 2050 emissions reductions targets), the other is to lower the floor (to cut compliance costs for companies). Which way this will go really all depends on the EU’s political will. Despite ambitious targets, the EU has already been softening-up on some climate regulations, including taking measures last month to reduce corporate reporting obligations and delaying CBAM. If the lowering-the-floor-ers win, potentially resulting in a lower carbon price, it could create headwinds for those trying to make headway in hard-to-abate sectors like cement and steel. There wouldn’t be as much of a price incentive to invest in cleaner technologies, if paying the fine is cheaper. You can see from the platform that there’s a large cohort of earlier-stage Industry startups in the EU who should be approaching FOAK, but a fragile ETS could hold back bets.

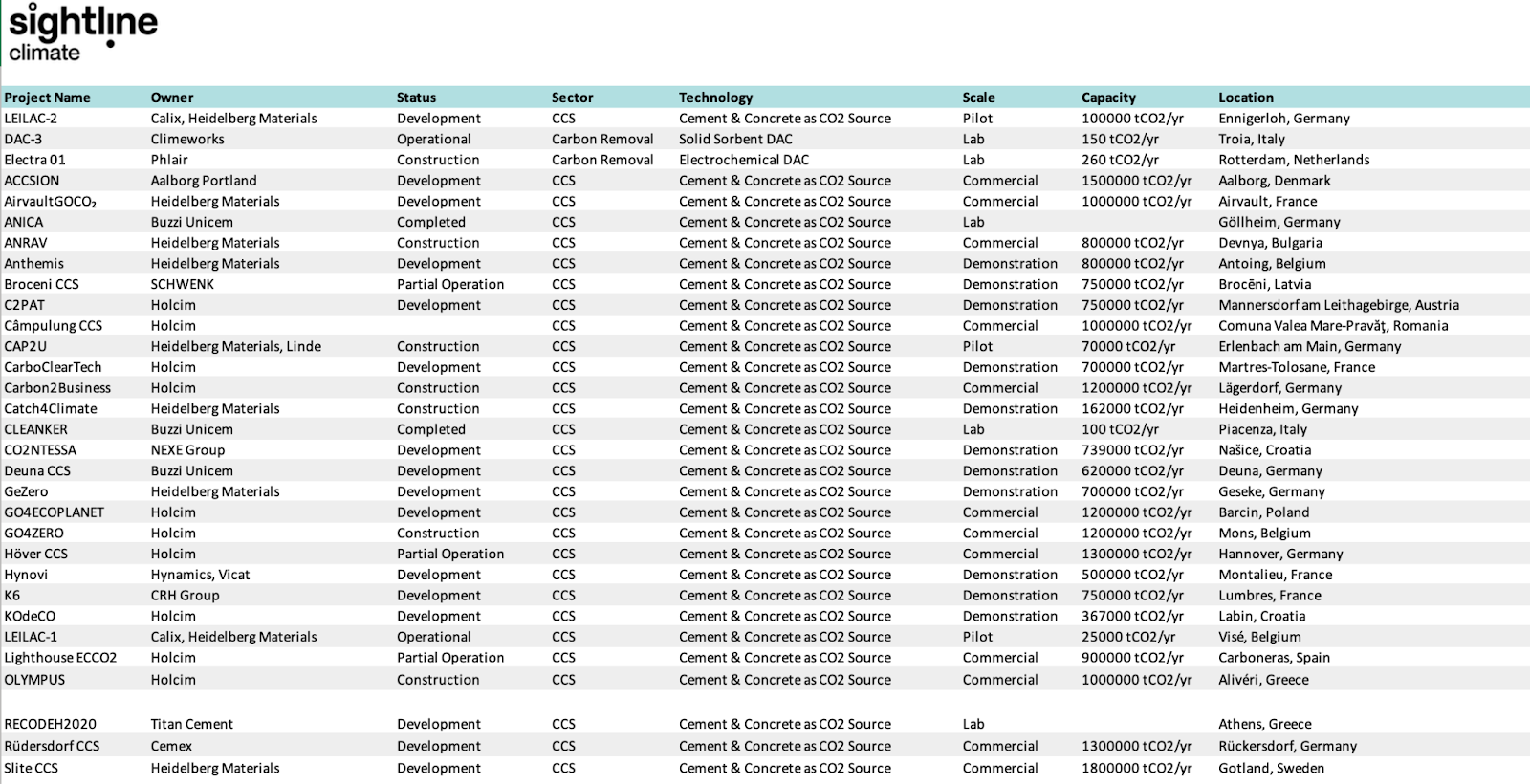

Tightening the cap, on the other hand, could push industrial emitters to strategically invest in low-carbon solutions for the long-term to avoid higher costs — and they can find such projects where these techs are getting implemented on the Sightline platform.

2. Offsets? Is the CDM back?!

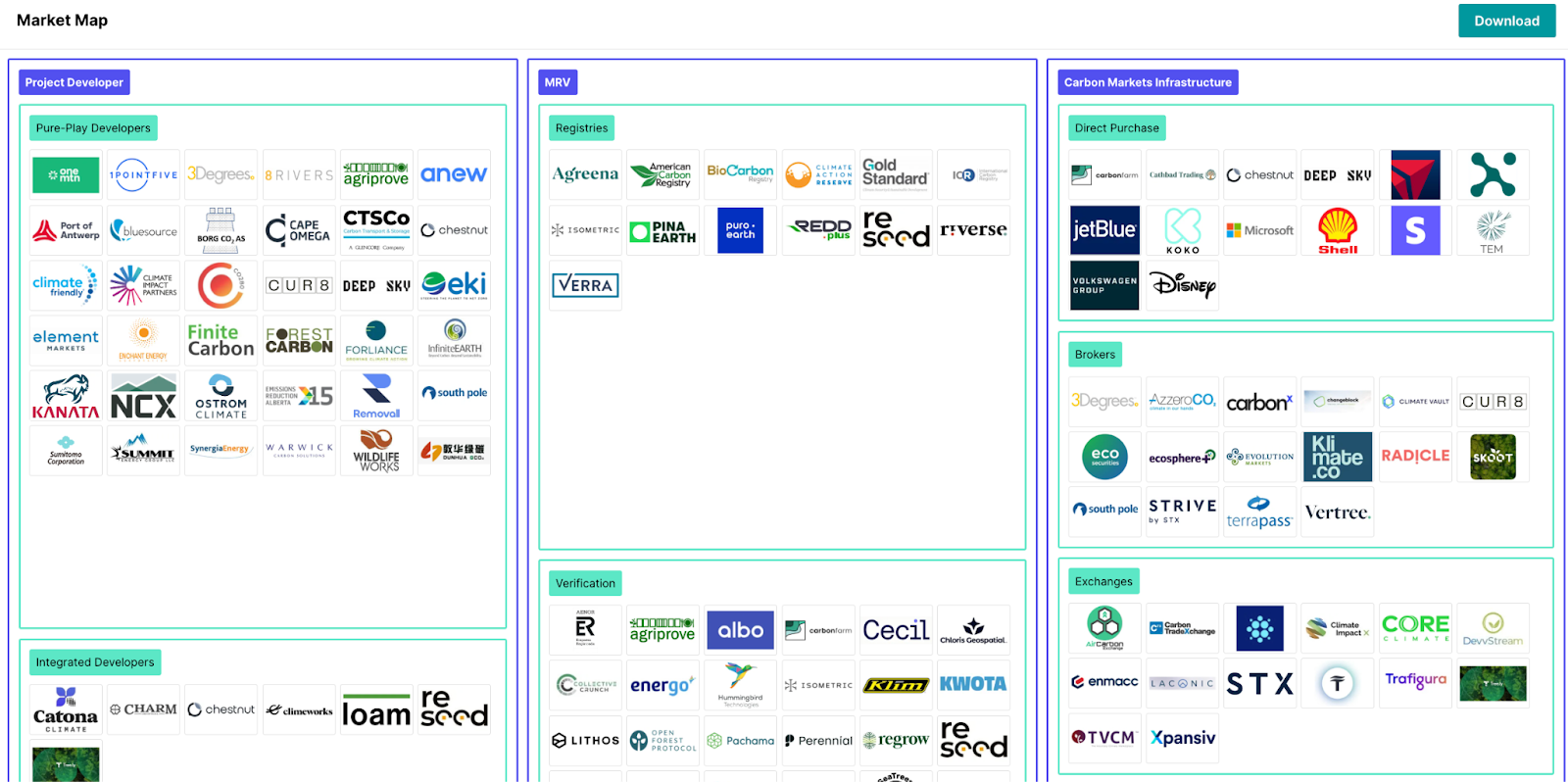

The ETS hasn’t included carbon offset credits since pre-2020, when it phased-out use of the UN clean development mechanism (CDM) program after credibility concerns. If offsets come back into the ETS, it probably won’t be the CDM specifically, but all those carbon removal project developers, verification, and carbon markets companies could have a real shot at riding a wave. But who could stand to catch the wave in this super-crowded line-up? Seems a bit early to tell, but see the market map below (and an even deeper version here).

3. And don’t forget about CBAM.

The EU's Carbon Border Adjustment Mechanism (CBAM) extends the ETS beyond EU borders, ensuring that imports face the same carbon costs as domestic producers. Like we said, implementation was delayed by a year, and it's currently in a transitional phase where importers must report the embedded emissions of their goods quarterly, but aren’t subject to any fines…yet. But the clock is ticking. Even with the delay, companies will still be accountable for their embedded emissions in 2026, and pay on those when actual payments begin in 2027. Sectors covered by CBAM include high-emission industries like cement, steel, aluminum, fertilizers, and electricity — industries that are particularly vulnerable due to their energy-intensive nature and exposure to global competition, making them key strategic priorities.

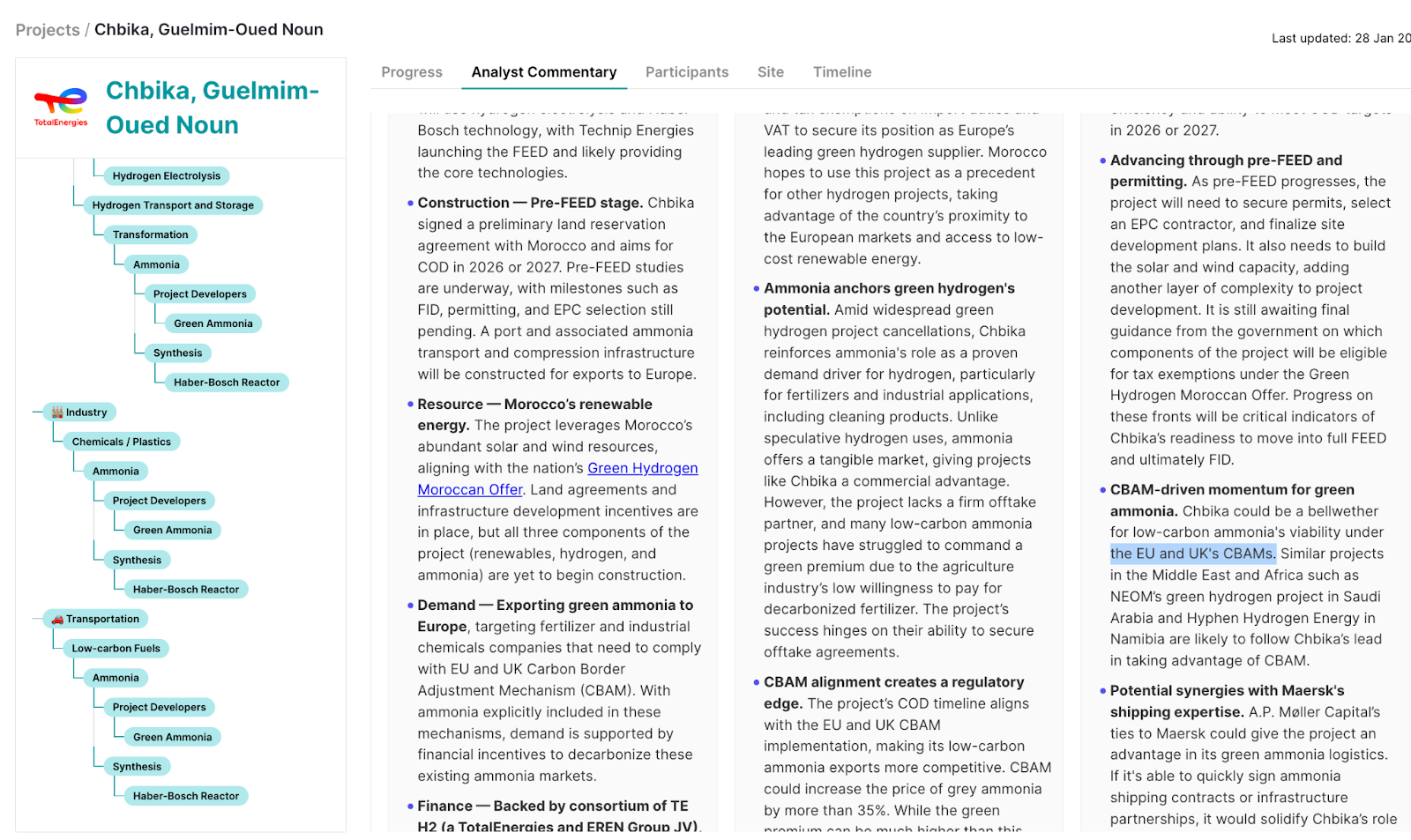

Some projects are specifically designed to take advantage of CBAM. We do case studies on important projects we call notable projects — see a case study on a CBAM-friendly project from TotalEnergies here. If CBAM stays intact, with real teeth, we’ll see more projects like this.